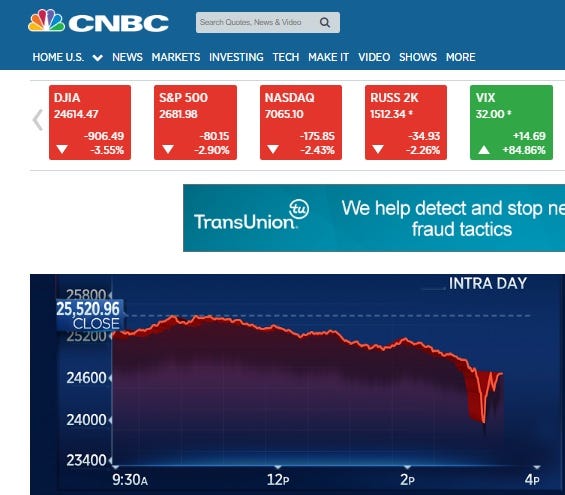

Dow plummets 1,500 -- that sure got your attention. Now, what to do?

Unless you are living under a rock, you now know that the stock market is in the middle of that time-honored tradition called a "correction" -- as in, months and months of tidy gains in your retirement account have been lost in just a day or two. At one point on Monday, the Dow was down more than 1,500 points, or more than 2,000 during two days. More important, everything gained during a very happy and fun 2018 has now been lost.

Now what?

I write this story now because you are probably paying a little more attention to your retirement accounts this afternoon, so while I have your attention, here's a few things you should know. And do. And not do.

DON'T OVERREACT

Most critically, you should not overreact. Whatever you've lost today, it's already gone. You can't fix that. You can make it worse by overreacting. Much worse.

SELL IF YOU REALLY WANT TO

That advice is usually followed by someone warning you not to sell. I won't do that, because it may very well be a wise step to sell some of what you're holding. It's a bad idea to do so because the Dow fell more than 1,000 points in one day. That's a terrible reason. But there can be good reasons for you to sell, too. Such as:

If you might need any of money you have invested in the short term, or even in the medium term (say, within the next 5 years, though reasonable person can bicker with that time horizon). You probably wish you had done this already, but that's ok. Do it now. You should NEVER invest money you need short-term in the stock market. Period.

If you really don't believe the economy will hold together under a Trump administration

If you think some of the individual companies you own are headed in a bad direction and will really suffer if the macro environment gets tougher. Another way of putting this: Lots of companies appear successful when the market is soaring, but that can be a mirage. If you own some of them, get out now.

If you feel like the Republican tax cut created something more like a sugar high than a fundamental stimulus for the economy

CONSIDER DOING WHAT I'M DOING

Me, I started selling off some of the stock-heavy mutual funds I owned in December, and sold quite a bit more in mid-January. But even there, I did what's called "taking some winnings off the table." I haven't stepped away from the poker game. As a 40-something person, I still have a majority of my retirement holdings in stocks. My time horizon is, hopefully, still measured in decades, so these gyrations will be long forgotten when I need that money. Still, I have sold (and turned into cash, or a few other conservative instruments) about 5% of my holdings a few times recently so I could "lock in gains" from last year's incredible performance. This is a strategy you should consider too.

DON'T TRY TO TIME THE MARKET

But please, please don't imagine you can time the stock market. You can't. Don't try to time the top. If you want to sell, sell now. Don't hope it'll bounce back to last week's high, and then sell. Just sell. You'll sleep better at night. If you have a very long time horizon, go ahead and buy; don't try to wait out this dip until it bottoms out. You can't do that either.

USE DOLLAR-COST AVERAGING TO SMOOTH OUT THE VIOLENT SWINGS

Instead, sell or buy in small pieces during the next several weeks, using what's called "dollar-cost averaging." That way the price you pay (or receive) will be smoothed out, and you'll suffer less from these day-to-day swings.

Don't worry if that sounds complicated; your company 401(k) or similar plan already does this for you, because you buy investments with every paycheck. If you chose to sell, you'll have to do that in pieces yourself. Don't sell all at once.

MAKE SURE YOU ARE INVESTING! DON'T PUNT TO SOMEONE ELSE

Most of all, make sure you are indeed saving for retirement. Make sure you are actively aware of how that money is invested. It's not enough to contribute to your 401(k). You have to know exactly HOW your 401(k) savings is invested. You are in the best position to make sure it's done well; no one else has your best interests in mind the way you do! (That would have been less true today, if the Trump administration hadn't strangled the fiduciary rule. Wish we'd all care more about anti-consumers changes like that instead of Stormy Daniels, but I digress.)

THE BEST WAY TO SAVE FOR THE FUTURE IS...SAVE! DON'T EXPECT MONEY FOR NOTHING

And don't forget what's really going on with today's market. Traders are trading, and they make money on volatility. All this action is good for them, even when it's bad for you. Computers are ticking stocks and derivatives up and down at the speed of light, and you are simply the raw materials for this computer game. Sometimes, you enjoy a side benefit of dividends or increased prices, sometimes you are a victim of them, but really, the best way to save for retirement is to actually make money and save it for retirement.

In the end, we all want to make money for nothing, but turns out that's very hard to do.

ORDER THE NEW EDITION OF GOTCHA CAPITALISM NOW! (Print edition also available)